24 Signs You’re in Financial Trouble — and How to Go from Financial Confusion to Clarity

Your Journey to Financial Maturity

Part 3: Avoidance, Excuses & Lack of Accountability (13–19)

Reading time: 10 min

Introduction: Your Journey to Financial Maturity

This is Part 3 of the 4-part series “Your Journey to Financial Maturity.”

In the previous stage, we explored how emotional spending and reliance on credit can create cycles of debt and frustration.

Now, we enter a more hidden challenge — avoidance.

This is where excuses, denial, and fear of facing the truth keep financial progress out of reach.

Avoidance is one of the biggest obstacles to financial recovery.

Ignoring bills, breaking budgets, or making excuses may protect your comfort in the short term, but it slowly erodes trust in yourself.

This stage is about facing reality — with honesty, discipline, and a willingness to take responsibility for your financial actions.

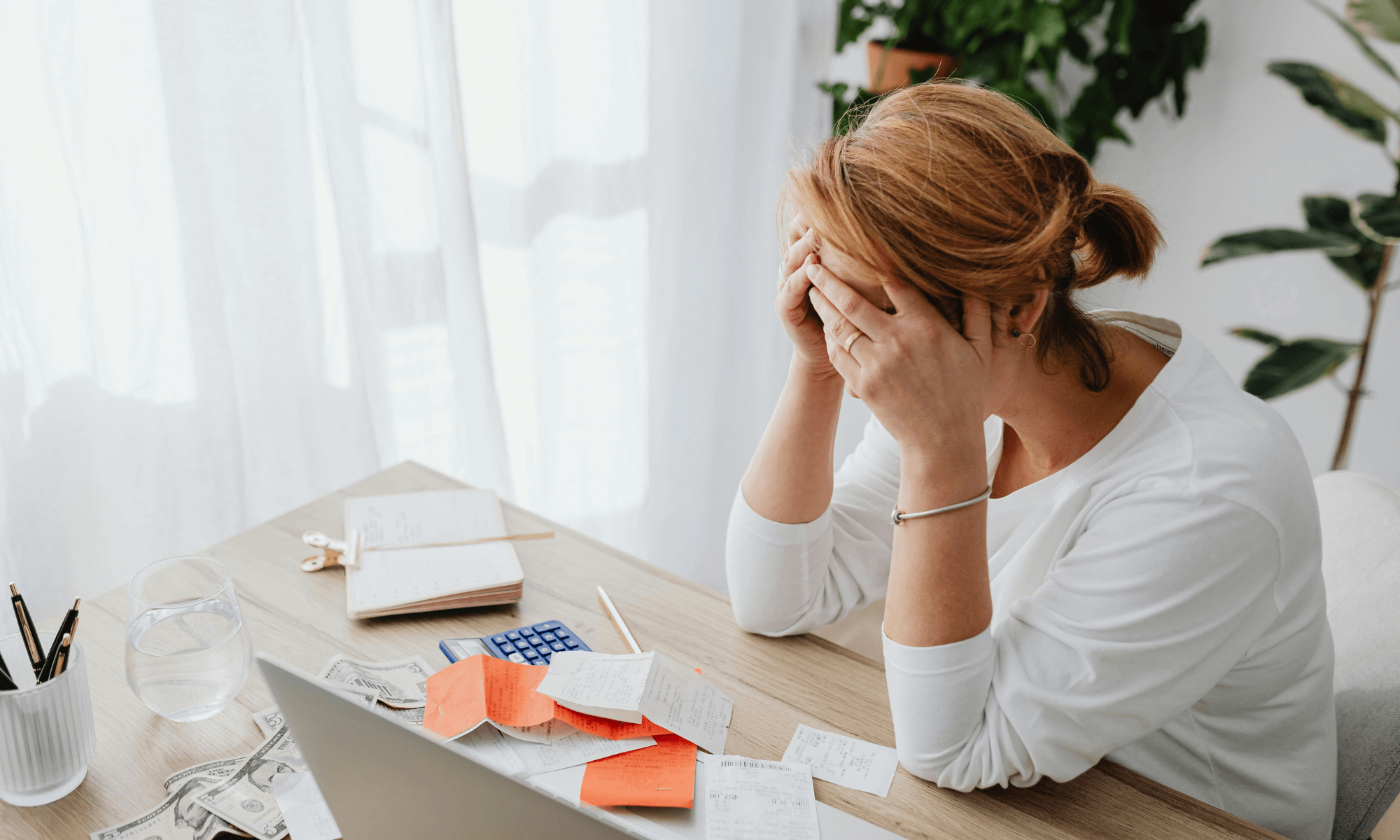

Many people feel anxious about checking their bank balance — and that’s completely human. But when that anxiety turns into avoidance, it becomes a silent form of self-sabotage.

Ignoring your finances doesn’t make the stress disappear; it only allows problems to grow unnoticed.

Avoiding your bank account often comes from fear — fear of seeing how little is left, fear of confronting bad habits, or fear of realizing how far you’ve drifted from your goals. So instead, you swipe your card and hope there’s enough. You avoid checking statements, delay looking at your balance, or ignore notifications from the bank.

But this emotional distance leads to practical damage: unpaid bills, overdrafts, and a false sense of control.

It’s like driving a car with your eyes closed — you might feel calm for a few seconds, but you’re heading straight into danger.

Facing your numbers regularly, even when it’s uncomfortable, is an act of courage and maturity. Awareness brings clarity. And when you know exactly where you stand — what’s coming in, what’s going out, and what needs attention — you regain control.

Start small: check your balance once a day or set weekly “money check-ins.” Over time, this becomes empowering rather than scary. The goal isn’t perfection — it’s awareness.

Some people don’t struggle because they lack money — they struggle because they avoid facing their finances.

Avoiding or delaying bill payments is one of the most common forms of financial irresponsibility. It often starts small: you forget to pay a bill once, promise to handle it tomorrow, or tell yourself you’ll deal with it when you “feel ready.”

Over time, this pattern turns into a habit of avoidance.

This behavior usually stems from stress, anxiety, or disorganization rather than a real inability to pay. You might delay opening bills because it feels uncomfortable — or because they remind you of financial obligations you’d rather not face. But every delayed payment adds up — late fees, penalties, and interest start eating away at your income. Eventually, you spend more just because you postponed what needed to be done.

Avoiding bills isn’t just a money issue — it’s an emotional one.

It’s about learning to face your responsibilities even when it’s uncomfortable. The solution begins with awareness: automate payments, set reminders, and schedule a “money check-in” once a week.

Facing your bills head-on builds confidence and replaces anxiety with control. You can’t fix what you won’t face — and once you start facing it, it becomes much easier than you imagined.

This is different from simply avoiding bills.

In this case, the money is there — but the priorities are misplaced.

You might have enough to cover your rent, phone bill, or credit card payment, yet you choose to spend it on something else: dining out, new clothes, or the latest gadget.

This isn’t about financial hardship; it’s about impulse and discipline.

Missing payments despite having the funds shows a lack of structure and long-term thinking.

It often reflects a mindset of “I’ll catch up later” — but later always comes with a cost: late fees, damaged credit, and unnecessary stress. It’s like saying yes to short-term pleasure while silently sabotaging your future.

The key here is accountability.

Before spending on non-essentials, ask yourself: “Have I paid what I owe first?”

Paying bills before spending is a simple but powerful habit that builds reliability and peace of mind.

The freedom to enjoy your money comes after you’ve met your responsibilities, not before.

If you constantly need to borrow money just to make it through the month — even though your income should be enough to cover your basic expenses — it’s a clear sign that something in your financial habits needs to change. Borrowing now and then can happen to anyone, but when it becomes a regular pattern, it usually points to overspending or poor money management.

It doesn’t matter whether you borrow from a bank, a credit card, or a friend — the problem is the same. Each time you rely on borrowed money to fill the gap, you reinforce the idea that you can always “fix it later.” But that “later” often never comes.

And if you’re borrowing from friends or family without paying them back promptly, the damage goes beyond money. It strains relationships, breaks trust, and can leave you without support when you truly need it.

People may start to hesitate helping in the future, leaving you without support in emergencies.

Financial responsibility isn’t just about budgets and numbers — it is also about integrity: keeping promises, being accountable, and respecting others’ money. A simple repayment plan, even in small installments, builds trust, strengthens relationships, and reinforces healthy money habits.

Hiding the truth about money — whether it’s lying about how you spend, concealing debt, or avoiding discussions about finances — is a major warning sign of financial irresponsibility.

When you share finances with a partner, spouse, or family member, your habits directly impact their money as well. Even small omissions, like not mentioning a loan or an overspend, can snowball into serious misunderstandings or tension. Over time, this lack of transparency can erode trust, making it harder to work together on financial goals or handle emergencies.

Avoiding conversations about money doesn’t protect you — it only delays the problems. Open communication about income, debt, bills, and spending habits is essential.

For example, if you’re struggling to pay off a credit card, sharing this openly allows you and your partner to create a plan together, rather than silently hoping it won’t matter. Similarly, discussing joint expenses or savings goals ensures that both parties are aligned and working toward the same priorities.

Being honest and proactive with finances also helps you develop personal accountability. When you face the reality of your spending, you are more likely to make deliberate choices rather than reactive ones. Financial clarity begins with conversation, and taking the first step to speak openly builds confidence. Not only does this protect your finances, but it also strengthens relationships and sets an example of integrity and responsibility.

Remember: honesty about money isn’t a weakness — it’s a tool for freedom. Every time you communicate openly about your financial situation, you reduce stress, prevent surprises, and take control of your future.

Start small if you need to — even sharing a weekly spending review or discussing one debt can make a big difference. Over time, transparency becomes a habit, empowering you and your loved ones to make better financial decisions together.

It’s one thing not to have any credit history or a low credit score because you haven’t taken out any loans or credit cards. It’s another if you already have loans or credit cards and aren’t paying them on time — or not paying them at all.

Maxed-out credit cards, late payments, or poor scores limit options and increase costs. Bad credit doesn’t just reflect a number — it’s a symptom of deeper financial habits like overspending, inconsistency, or lack of planning.

It can make future borrowing expensive or even impossible, and it often signals to lenders that you’re not managing your finances responsibly.

But a low score isn’t permanent — it’s feedback. Responsible credit use, on-time payments, and gradual debt reduction can rebuild your score over time.

Improving credit is really about improving habits — discipline, consistency, and awareness — all of which strengthen your overall financial health.

One of the most dangerous financial mindsets is believing that more money is coming soon.

Maybe you expect an inheritance, a bonus at work, a pay raise, tax refund, or even birthday money — and in your mind, that future windfall will magically fix everything. But what if it never comes? Or it’s less than you imagined?

Relying on uncertain money creates a false sense of security and leads to procrastination. You might delay paying off debt, skip saving, or ignore your budget because you believe the “big payday” will cover it all.

In reality, this thinking keeps you stuck — waiting instead of acting.

The truth is, no windfall can fix habits built on avoidance. Even if that extra money does arrive, it often disappears quickly because the underlying behaviors haven’t changed.

Instead, take charge now: start saving regularly, cut unnecessary expenses, and make consistent progress on your debts.

Financial stability doesn’t come from luck or timing — it comes from intentional, everyday choices that put you, not chance, in control.

This was Part 3 of “Your Journey to Financial Maturity” — Avoidance, Excuses & Lack of Accountability.

In the final stage, we’ll explore Growth, Mindset & Financial Maturity, where you’ll learn how to rebuild trust with yourself, shift your mindset, and create lasting financial confidence.