How Higher Rental Taxes Might Affect Iceland’s Housing Market: A Move That Could Backfire?

Reading time: 25 min

Introduction

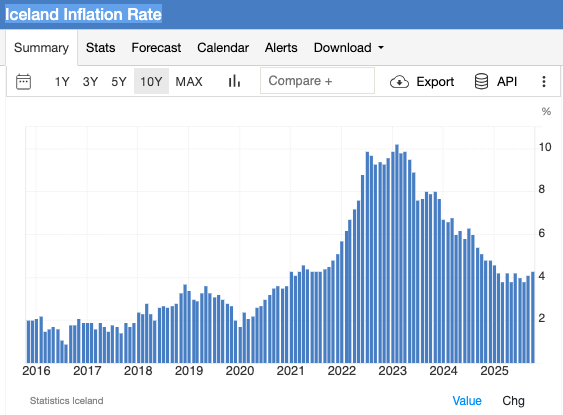

Iceland’s housing market is in a difficult place. Rents keep rising, construction is too slow, inflation is still around 4%, interest rates remain painfully high and homeownership is increasingly out of reach.

Under the current system in Iceland, 50% of rental income is tax-free, and the remaining 50% is taxed at 22%, resulting in an effective tax of 11% for long-term landlords.

The government has now proposed reducing the tax-free share from 50% to 25%, meaning 75% of rental income would be taxed. This raises the effective tax from 11% to 16.5% — a 50% increase.

Some view this as a way to make the system “fairer” or generate more revenue. But in reality, increasing taxes on long-term rentals risks making the housing situation worse — for renters, landlords, and the overall economy.

To understand why, we need to look at how Iceland’s housing ecosystem actually works. Taxes, supply, demand, construction costs, interest rates, inflation, immigration, tourism, and regulation all interact. None of these factors exist in isolation. And unless Iceland addresses the root causes of the housing shortage, increasing rental taxes may deepen the supply gap and push prices up even faster.

Before we dive in, I want to be clear about something: I am writing this article based on the best available information today. I have no political agenda, no personal connections to banks or interest groups, and no hidden motives.

This is simply a topic I enjoy exploring — connecting details to the bigger picture and learning from the past — and I want to explain it in a way that’s accessible and easy to understand for everyone.

Let’s start with supply and demand.

Raising taxes on long-term rental income makes renting less profitable for landlords. When returns decrease, many property owners naturally reconsider whether long-term renting is still worth the effort — especially given the responsibilities, regulations, and risks involved in being a landlord in Iceland.

While it’s uncertain exactly how much the tax increase will reduce supply, several likely responses can be expected:

1. Considering property sales or alternative investments:

Some landlords may explore selling their property or investing in alternatives that offer better returns. If renting no longer justifies the cost, time, and legal responsibilities, selling becomes a realistic option.

2. Temporary shifts to short-term rentals:

Another group may take their property off the long-term market and instead rent short-term through Airbnb or similar platforms for a few months, staying under the regulatory limits (e.g., 90 days or 2,000,000 ISK in revenue). While this can help landlords cover costs, shifting units out of the long-term supply for several months disrupts market stability — and reduces the number of available homes for residents.

3. Higher rent to offset costs:

When long-term rental supply shrinks — whether because landlords exit the market, switch to short-term rentals, or face higher taxes and operating costs — but demand stays the same or increases (driven in part by population growth, which I expand on later), rents naturally rise.

Landlords adjust prices to cover higher expenses, and tenants end up absorbing the impact. In Iceland’s already strained housing market, even small drops in supply can trigger sharp rent increases, making an already expensive system even less affordable.

Whenever the government introduces a tax increase, people naturally adjust their behavior to minimize its impact.

One of the most immediate reactions to sudden policy changes is pre-emptive rent increases. When landlords feel blindsided or targeted by new rules, many lose trust in the stability of government policy. This uncertainty often leads them to raise rents — sometimes even more than the actual tax increase would require — as a way to protect themselves from future changes they fear may be coming next.

In a small and sensitive market like Iceland’s, this fear-driven behaviour can accelerate rent inflation and make housing even less affordable for tenants.

Another common response is for landlords to impose stricter requirements on renters. This may include larger deposits, more documentation, and tighter lease conditions, all intended to offset the perceived risk of higher taxes or further regulation. While this protects landlords, it raises barriers for tenants who already struggle to enter the rental market.

A more troubling reaction is the shift toward underreporting rental income or moving into informal, “under-the-table” arrangements. This often involves accepting cash payments without formal contracts or proper tax reporting. Such practices reduce transparency and weaken oversight of the housing sector.

This shift in behavior can have several consequences for the economy and society:

1. Reduced tax revenue:

When income is underreported or unrecorded, the government collects less money than expected.

2. Distorted housing market:

Informal rentals make it harder to track actual supply and demand, complicating policy decisions and potentially worsening rental shortages.

3. Higher administrative costs:

Tax authorities may need to spend more resources detecting and managing “under-the-table” rentals, reducing overall efficiency.

In short, if landlords begin to feel punished or uncertain about future policy, a higher rental tax can create behavioural responses that undermine its purpose. Instead of stabilizing the market or improving affordability, it risks raising rents unnecessarily, pushing activity underground, and weakening trust between landlords and the state — a clear example of short-term gain becoming long-term pain.

If long-term rental income is taxed more heavily, rental property becomes less attractive as an investment. Many landlords may redirect their money into safer or more convenient options like high-yield savings accounts, bonds, index funds, or foreign investments.

Rental housing already carries significant responsibilities — managing tenants, handling repairs, navigating regulations, and dealing with vacancy risks. If the tax advantage disappears, so does much of the incentive.

Landlords may start asking themselves: “Why should I rent out my apartment when I can earn comparable — or even slightly lower — returns by simply keeping my money in a high-yield savings account, stocks, dividends, or index funds, all with far less stress and uncertainty?”

If enough people reach that conclusion, the long-term rental supply could gradually shrink. In some cases, Icelandic capital may even shift away from the housing market — or out of the country entirely.

That’s a worrying scenario for a small, inflation-sensitive economy already struggling with limited housing availability.

Now, let’s talk about an issue that does very little to help first-time buyers.

Mortgage interest rates in Iceland remain extremely high. Non-indexed loans currently sit around 8–10%, depending on the loan type (I explain the different loan options later in the article). At these levels, a large share of each monthly payment goes toward interest, especially in the early years. Even households that manage to save for a down payment often find that the cost of borrowing makes homeownership out of reach.

Raising taxes on rental income does nothing to address this. Higher taxation simply increases the cost of renting, while the real barrier to buying a home — high interest rates — stays exactly the same.

The Central Bank of Iceland also plays a major role through its debt service limits, which restrict households to spending 35–40% of their net income on mortgage payments — 35% for first-time buyers and 40% for others. These caps determine how much people can borrow, regardless of what they currently pay in rent.

Meanwhile, the average rent for an 80–90 m² apartment in the capital is around 350,000 ISK per month — a very high figure. For context, in 2024 the average monthly salary for full-time employees was 845,000 ISK before tax, with a median of 753,000 ISK.

If renters are already required to spend such a large share of their income just to secure a place to live, it raises an important question:

Shouldn’t the same percentage be considered acceptable when evaluating mortgage affordability for first-time buyers?

Put differently: if renters can reliably pay 350,000 ISK to a landlord every month, why shouldn’t they be allowed to put that same amount toward a mortgage?

And here’s the deeper issue: while the 35–40% rule makes sense in many countries where rent levels are comparatively low, Iceland’s housing market is an outlier. Rent here often exceeds that threshold for ordinary earners. In such cases, a strict debt-service cap may unintentionally trap people in the rental market — forcing them to pay far more in rent than they would pay on a mortgage, simply because the rules don’t reflect Iceland’s unusually high rental costs.

A more flexible approach — one that takes into account what households are already managing to pay each month — could make homeownership more accessible without compromising financial stability.

High interest rates affect far more than homebuyers — they also hit developers and contractors.

When borrowing becomes expensive, building new apartments becomes less appealing, so construction slows. As a result, the housing supply fails to grow at the pace Iceland urgently needs.

With too few new homes entering the market, the long-term rental supply remains tight and rents keep rising. In short, high interest rates slow the growth of the housing stock, worsening affordability for renters and deepening Iceland’s long-standing housing shortage.

One of the long-term consequences of Iceland’s high mortgage rates, rising property prices, persistent inflation, higher property and rental taxes, and strict regulations is that both tenants and landlords may start questioning whether living in Iceland is financially sustainable.

For tenants, soaring rents and increasing living costs make it harder to achieve stability or save for the future.

For landlords, shrinking profit margins, heavier tax burdens, and tighter regulations reduce the appeal of property ownership.

When these pressures combine, it’s understandable that more people might consider moving to more affordable countries, where housing is cheaper and long-term financial planning feels more predictable.

In Iceland, gains from the sale of a primary residence are tax-free if the property has been owned by the taxpayer for at least two years and is within certain size limits. If the residence has been owned for less than two years, the gains may be rolled over through a reduction in the acquisition cost of another private residence, and taxation of such gains may be deferred for up to two years.

This relatively short holding period encourages short-term speculative buying: people can purchase a home, live in it (or register it as their residence) for just two years, and then sell it tax-free, treating real estate more like a short-term investment than a long-term home.

Such behavior has increased transaction frequency and contributed to higher assessed property values, which in turn raises property tax revenues, while simultaneously reducing the availability of homes for long-term residents. Higher housing costs also put upward pressure on overall living expenses in Iceland.

By contrast, many European countries require longer holding periods, often 3–5 years or even up to 10 years, to qualify for tax exemptions, which discourages short-term flipping and speculation.

Immigration has been a major driver of population growth in Iceland.

Even if mortgage rates fell tomorrow or rental taxes stayed the same, the country would still face a serious housing shortage, because population growth has consistently outpaced construction.

In recent years, thousands of foreign workers, students, young people, and asylum seekers have moved to Iceland. While this strengthens the labor force and benefits the economy, it also creates a structural challenge: thousands of new households need homes, but the housing market is too small to meet that demand.

When demand rises faster than supply, prices naturally increase, putting pressure on renters, first-time buyers, and policymakers alike. This isn’t about greed or speculation — it’s basic economics. Tax policy alone cannot solve this imbalance; it must be paired with measures that coordinate immigration, labor demand, and housing construction.

To understand why interest rates in Iceland remain relatively high today, we need to look at the lingering effects of policies and market behaviors during the COVID years.

Below, I list five key factors that explain how decisions made during COVID continue to influence inflation, housing demand, and today’s high-interest-rate environment.

When the pandemic hit, the Central Bank of Iceland — like many central banks worldwide — cut interest rates sharply. Borrowing suddenly became much cheaper, making mortgages more accessible. As a result, many households took the opportunity to buy property, with some even purchasing multiple homes, upgrading to larger homes, or refinancing existing loans.

This surge in housing demand, combined with already limited construction and a small housing market, contributed to rising prices, growing household debt, and inflationary pressures. Even years later, the effects of these decisions are still felt, and this rapid increase had several consequences:

With cheap credit widely available, real estate prices rose sharply across the country:

Residential Property Market Price Index in Iceland (whole country, total), 2016–2025. Source: TradingEconomics.com.

What happens when property values rise?

When property values increase, the assessed value of a home (fasteignamat) rises, which directly leads to higher property taxes.

When landlords face higher property taxes — and that’s before even considering higher rental taxes — they often pass some of the costs onto tenants through increased rent. Even moderate increases across the rental market can collectively put pressure on household budgets, affect the broader economy, and contribute to inflationary pressures.

Then, we have the CPI (Consumer Price Index), which measures changes in consumer prices, and inflation is derived from these changes.

In Iceland, housing is the largest component of the CPI, giving it the strongest influence on the country’s inflation:

Annual CPI Component Changes in Iceland, October 2025. Source: Statistics Iceland.

Because housing makes up such a large share of household expenses, it plays a major role in how inflation is measured — and it becomes a key factor to address when trying to bring inflation down.

So, when housing costs rise — whether due to higher property taxes, higher rents, or both — the effects ripple through the economy:

1. Direct impact on inflation:

Higher housing costs increase the cost of living, causing inflation to rise.

2. Reduced disposable income and demand pressures:

As households spend more on housing, they have less money for saving, investing, or purchasing other non-essential goods and services.

Spending shifts toward necessities like food, transportation, and everyday services, which can put upward pressure on prices in these areas.

In other words, higher property and/or rental taxes do more than just raise rents — they trigger a chain reaction that amplifies inflation across the economy, raising prices in multiple sectors.

This is how rising housing costs indirectly fuel broader inflation.

Consumer Price Index (CPI) in Iceland, 2016–2025. Source: TradingEconomics.com.

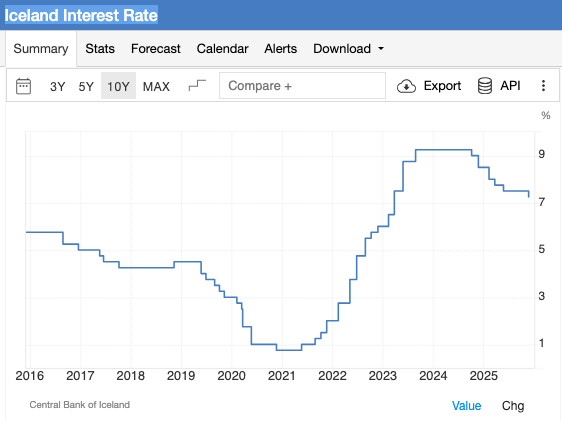

To fight inflation, the Central Bank of Iceland shifted from ultra-low interest rates to rapid and aggressive hikes:

Central Bank of Iceland Key Interest Rate, 2016–2025. Source: TradingEconomics.com.

Homeowners who bought during the low-rate period (roughly 2020–2021) benefited from those low rates and had temporary breathing room — but only for a short time, because in Iceland, mortgages can typically be fixed for 3 years, or at most 5 years.

As a result, many of these loans from 2020–2021 have already reset, are currently resetting, or will soon reset in today’s high-interest-rate environment.

Fixed rates for non-indexed mortgages are now around 8–10%:

Fixed Mortgage Rates in Iceland, 2020–2025. Source: Landsbankinn.

If borrowers don’t refinance, the loans automatically switch to variable rates — typically around 9–10%, depending on the financial institution, loan type, and loan-to-value ratio:

Variable Mortgage Rates in Iceland, 2020–2025. Source: Landsbankinn.

As we can see, this is a big jump compared to the ultra-low rates available during COVID.

When these low-rate loans reset to much higher interest levels, the financial pressure on households rises sharply. Most property owners try to hold onto their homes and absorb the pressure rather than sell immediately — especially if they buy the property as a long-term investment.

Many landlords pass some of these higher costs onto tenants through increased rent, contributing to inflation and reducing affordability.

Other common consequences include delayed maintenance, upgrades, or renovations.

In some cases, landlords decide to sell when the financial strain becomes too great. However, given Iceland’s tight rental market and strict lending rules, it remains unclear whether these sales meaningfully increase housing supply or reduce rents overall.

Buyers entering the market from 2023 onward have faced high interest rates from the start, making mortgage payments extremely difficult to afford. As a result, many buyers who intended to purchase a home — and still plan to — can no longer afford these expensive loans or qualify for them.

Consequently, many households have been effectively locked out of homeownership and are forced to stay in — or return to — the rental market. This adds pressure to an already limited rental supply, driving rents higher, particularly in the capital area.

This chart shows how new mortgages in Iceland have shifted since 2013.

What stands out most is the major change after late 2022: as inflation rose and interest rates on non-indexed mortgages climbed to 8–10%, households began taking far more indexed loans than before.

Shift to Indexed Mortgages in Iceland 2013–2025, showing the surge in indexed loans after late 2022.

Source: HMS (Icelandic Housing and Construction Authority), Monthly Report, November 2025

For readers unfamiliar with Icelandic mortgages, Iceland has two main types of mortgage loans:

1. Non-indexed loans (óverðtryggð):

These are the standard (“normal”) loans where the principal does not increase with inflation, so that you can see the balance going down each month. However, once inflation surged in Iceland in late 2022, interest rates on these loans jumped to about 8–10%, making monthly payments extremely high from the start — often too high for many households to manage or to qualify for under the Central Bank’s 35–40% income rule.

2. Indexed loans (verðtryggð):

These loans are directly linked to inflation. In most countries, such loans either don’t exist, are considered too risky, or are outright banned — but Iceland still allows them. With these loans, financial institutions shift the inflation risk entirely to the borrower. In other words, verðtryggð loans protect the financial institution from inflation, not the consumer — the borrower carries all the inflation risk.

Although the interest rate on indexed loans may appear low on paper (for example, 2–4% in bank charts), the principal is adjusted for inflation. This means that even if borrowers make all their payments on time, the loan balance grows rather than shrinks. During periods of very high inflation, this adjustment can sometimes cause the balance of some indexed loans to increase significantly over a few years, making them far more expensive than they initially seem.

The main appeal of indexed loans is their lower initial monthly payments, which often makes them the only realistically affordable option for many households in today’s high-interest environment.

There are two main reasons why so many people opted for indexed loans:

1. High interest rates on non-indexed loans for new buyers:

New homebuyers entering the market from late 2022 onward faced non-indexed rates around 8–10%, pushing monthly payments beyond what most households could afford or qualify for. Indexed loans, however, offered lower starting payments and became the only manageable option for many.

2. Expiration of cheap fixed-rate loans from 2020–2021, affecting existing homeowners:

During COVID, many households locked in very low rates for 3–5 years. These fixed periods, however, began ending in 2023 and will continue through 2027, exposing borrowers to today’s high rates upon refinancing. Again, many opted for indexed loans due to the lower monthly payments or because they could not qualify for non-indexed loans under the Central Bank’s rules.

What this means:

As of September 2025, 65% of all mortgages are indexed (verðtryggð), while only 35% are non-indexed (óverðtryggð). Overall, about 60% of bank housing loans to households and 74% of pension fund housing loans are indexed.

The reason why indexed loans are risky in a high-inflation period:

– debt grows every month, even if all payments are made on time,

– a larger share of payments goes toward interest rather than reducing the principal,

– it takes much longer to build equity in the home.

This also creates a serious long-term risk — risk of negative equity:

If the loan balance grows faster than the property value, homeowners can end up owing more than their home is worth, making refinancing, selling, or moving difficult without taking a financial loss.

Consequences of indexed loans, high interest rates, and higher taxes:

Indexed loans, high interest rates, and higher taxes are interconnected and form a chain: as landlords face rising costs, many pass some of these expenses onto tenants, pushing rents higher. Higher rents, in turn, contribute to inflation, reducing households’ disposable income and affecting spending across the economy. A cycle that puts continuous pressure on the housing market, creating a feedback loop that impacts renters, homeowners, and the broader economy.

Whenever prices rise — whether for rent, food, or fuel — people naturally ask: “Why doesn’t the government just limit prices?”

At first glance, it seems simple: cap rents if they’re too high, freeze fuel prices if they spike. But in reality, price controls usually cause more problems than they solve.

Here’s why.

Price controls generally come in two forms:

Price ceilings set a maximum a product or service can cost — like rent control or fuel caps.

Price floors set a minimum price — such as minimum wages or minimum alcohol pricing.

While these policies are often well-intentioned, they interfere with the natural balance of supply and demand, distorting markets and creating inefficiencies or shortages. When prices can’t move freely, they stop signaling true scarcity or demand.

Take rent control as an example: initially, tenants benefit from lower rents, but over time landlords may lose the incentive to maintain properties or invest in new rental units. Developers may build fewer apartments because profits shrink, eventually reducing the overall rental supply. Informal “under-the-table” renting often increases, leaving tenants with fewer protections.

The key point is this: prices themselves are not the enemy. They are signals guiding economic decisions — rising prices tell producers, “We need more of this,” prompting construction or increased production. Falling prices signal excess supply, discouraging overproduction.

When governments freeze or manipulate prices, these signals vanish, and the market cannot adjust naturally. Over time, this creates hidden problems — shortages, declining quality, and inefficient allocation of resources.

Iceland doesn’t need frozen prices. It needs more housing, better planning, and policies that tackle the root causes. By focusing on expanding supply, increasing productivity, and supporting those most affected, the government can deliver real, sustainable relief without creating unintended consequences.

1. Increase housing supply

The main driver of high rents and property prices in Iceland is a shortage of housing.

To address this, policymakers should:

– Speed up building permits and zoning approvals to reduce delays and costs, while maintaining quality standards.

– Encourage private developers to build affordable housing through partnerships, tax incentives, or construction subsidies.

– Promote modular and energy-efficient construction, which is faster and cheaper.

– Build apartments that meet residents’ needs — including parking and other features that families or commuters require.

– Offer tax incentives for long-term rentals, encouraging landlords to keep properties on the rental market.

Focusing on building more of the “right kind” of housing — not just more units — will help ensure supply begins to match demand and relieve pressure on both rents and prices.

2. Make homeownership more accessible for first-time buyers

High mortgage rates and strict lending rules prevent many renters from buying, even if they already pay high rents.

Policies should better reflect real affordability:

– Reconsider the Central Bank’s rule that mortgage payments cannot exceed 35–40% of net income for first-time buyers.

Allowing them to allocate the same portion of income they currently spend on rent toward mortgage payments would make homeownership more achievable.

3. Extend the tax-free period for selling homes

Currently, homeowners may qualify for tax-free gains on the sale of a private residence if it has been owned for at least two years and meets certain size limits. This short holding period encourages short-term speculation, contributing to higher property turnover and rising prices.

Extending the holding period — for example, to five years, as is common in many European countries — could help create a more stable and predictable housing market by:

– Reducing short-term flipping and speculative buying.

– Stabilizing property prices and property tax assessments.

– Encouraging long-term ownership and investment in housing.

A longer holding period would curb speculation, support price stability, promote property maintenance, and provide families with greater security and long-term stability in their homes.

4. Align population growth, tourism, and housing capacity

Population growth, combined with high demand for short-term tourist rentals, is putting additional pressure on housing availability.

Coordinating labor, immigration, tourism, and housing policies is essential to ensure that demand and supply are better balanced.

5. Strengthen economic and financial education — and improve clear communication

A well-functioning housing market also depends on informed households.

Many people in Iceland don’t fully understand how indexed loans work, how rising interest rates affect them, or how inflation impacts their daily expenses. This lack of understanding makes families more vulnerable to risky decisions and allows poor policies to go unchallenged.

Improving financial literacy would help:

– Renters understand the true long-term cost of renting versus buying.

– Homebuyers understand mortgage types, risks, and interest-rate cycles.

– Citizens understand how taxes, government spending, and inflation interact.

– Policymakers face better-informed public pressure to design smarter policies.

Financial education only works when the government communicates clearly. Icelandic institutions need to explain policy decisions, housing strategies, and long-term plans in a transparent, consistent, and accessible way — helping people understand why policies are made and how they affect households.

As you can see, Iceland’s housing crisis is complex and interconnected.

Looking at the issues discussed above, it’s clear that Iceland is now dealing with the aftermath of past decisions.

Easy access to cheap credit fueled rapid apartment price increases. Higher prices then led to increased property taxes, while the two-year tax-free rule encouraged short-term speculation. Together, these factors added to overall inflation, creating a cycle that continues to put pressure on Iceland’s housing market.

Many of the pressures we see today — high rents, unaffordable mortgages, and stressed tenants and landlords — are direct consequences of these past choices.

The purpose of this article is to give a clear, simplified overview of Iceland’s housing crisis — its causes, its consequences, and how everything is connected. You don’t need to be an economist to understand every point in this article, but hopefully the bigger picture is now much clearer. Of course, this isn’t a complete list of solutions — other factors, such as government spending or wider economic policies, could each warrant 10–15 pages of detailed analysis on their own.

If you found this article helpful, share it with a friend or spread the knowledge. Understanding the system is the first step toward meaningful change, and learning from past mistakes is the best way to create a more stable and fair housing market for everyone.