How to Protect Yourself Financially in Uncertain Times

(And What to Do If You Just Lost Your Job)

Reading time: 25 min

Introduction

If you’ve just been laid off or you’re worried about losing your job, you are not failing. You are experiencing something millions of people go through whenever the economy contracts.

A recession is not a personal flaw. It’s a cycle — and cycles have an end.

This guide is designed to help you navigate this period with clarity and confidence.

PART 1:

Preparing for Uncertain Times While You Still Have a Job

Economic uncertainty is part of life, but the way you respond to it can make all the difference.

Even before a layoff happens, there are several key steps you can take to protect your financial stability.

Preparation is about foresight, not fear.

Recessions are not just numbers on a chart. They change the psychology of a whole society. People buy fewer things, delay big purchases, cancel travel, and prioritize essentials. Companies, feeling the pressure from reduced consumer spending, respond by cutting costs — often through layoffs, hiring freezes, and restructuring.

This creates a chain reaction: less income → less spending → more pressure on companies → more layoffs.

During these periods, even excellent workers can lose their jobs, and even responsible people can struggle financially. The economy is not punishing you personally; it is simply shifting. Once you see it this way, you stop taking things as a personal failure and start acting strategically.

Recessions also tend to increase emotional stress. Fear of the unknown makes people worry about paying bills, keeping their homes, or rebuilding their careers. Understanding this emotional layer is important, because fear-driven decisions often hurt people more than the recession itself. Staying calm, informed, and proactive is your biggest advantage.

Hiring freezes often signal a slowdown before layoffs hit:

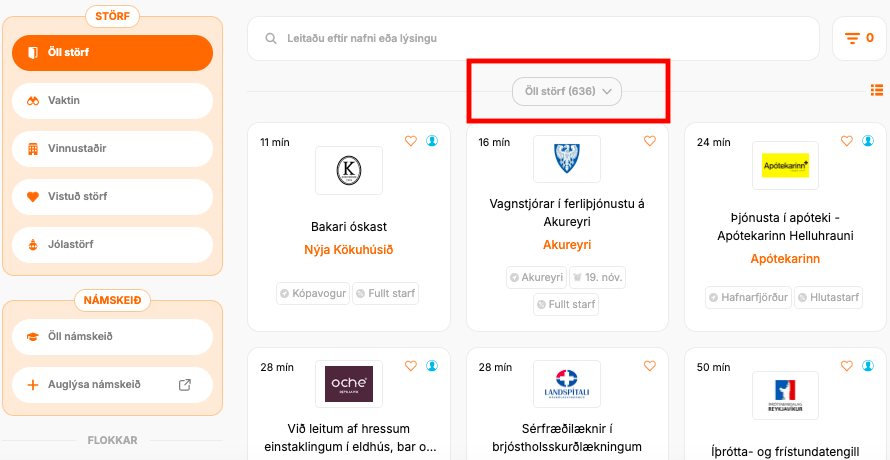

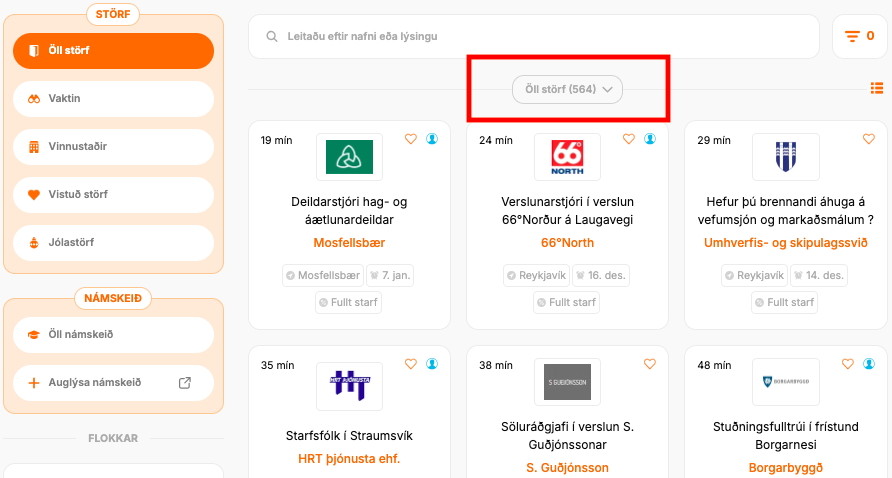

The economy is cooling down, and one of the clearest signs I’ve noticed is that job opportunities are steadily decreasing. For example, on one of Iceland’s most common hiring platforms, the number of job postings has been declining month by month. Previously, it wasn’t unusual to see over 900–1,000 vacancies. By early October 2025, that number had dropped to around 770, then to 636 at the start of November, and down to 564 in early December.

Part of this decline may be seasonal — companies often pause hiring toward the end of the year and postpone new positions until the following year. Even so, the drop is significant enough to highlight that opportunities are becoming scarcer, and it’s a trend worth noting.

Available job postings in Iceland, beginning of November vs. beginning of December 2025. Source: Alfred.is.

The thing is, many people expect layoffs to be the first sign of a slowdown, but in reality, hiring freezes usually come first. Layoffs often follow later, when companies feel the need to cut costs.

It can feel uncomfortable to think about, but having a backup plan in case your income stops is essential. Even if your job feels secure today, unexpected changes can happen — and mentally preparing for them will make you far more resilient.

Start by asking yourself a few questions:

* “What would I do if I lost my job tomorrow?”

* “Could I generate a second income, even a small one, from my skills or hobbies?”

* “How much do I have in an emergency fund? Is it fully funded?”

* “How is my debt situation? What types of debt do I have, and what are the interest rates on each?”

* “Where can I cut back on my expenses now so I can use that money to fully fund my emergency fund or pay down high-interest debt?”

For example, you might consider teaching yoga, offering coaching, taking on freelance projects, selling artwork or photography, or teaching languages like Icelandic or English to generate a second income. Think about what you’re good at and how you could turn those skills into income if necessary.

Main takeaway:

You don’t need a perfect plan or a complete overhaul yet — the goal is simply to start thinking about cash flow and savings.

Having a few alternative options in mind gives you control, reduces panic, and prepares you to act decisively if circumstances change.

Even if your job feels secure today, uncertain times can come unexpectedly. Reducing your debt now gives you more freedom, flexibility, and control before a crisis hits.

Debt — especially high-interest debt — acts like a ticking time bomb. The payments don’t stop when your income slows down, and that’s exactly when debt can spiral out of control.

Ask yourself:

* “What debts do I currently have?“

* “Which ones carry the highest interest rates?“

* “How can I start paying them down before they become a problem?“

Prioritize high-interest debt first:

For debts outside Iceland, focus on anything above 7%, and in Iceland, target debts with interest rates around 10% or higher. These typically include personal loans, credit cards, and car loans. Your main focus should be paying down high-interest debt as quickly as possible while maintaining minimum payments on the rest.

Mortgage debt is different:

If your mortgage interest rate is fixed at around 5% or lower outside Iceland, or around 6–7% or lower in Iceland, there’s no need to panic or rush to pay it off — just make sure you know exactly when your fixed period ends.

Avoid lifestyle upgrades, like buying a bigger home or a new car. Now is the time to prioritize financial stability, not appearances.

By actively reducing your debt while still employed, you’re creating a financial buffer. This buffer lets you handle unexpected changes — whether that’s a slowdown at work, rising costs, or a sudden emergency.

Key takeaway:

Preparing today means more choices tomorrow. Get ahead of the game — reducing debt and planning your finances now gives you flexibility, options, and control when uncertainty hits.

When the economy gets shaky, companies naturally start looking at their costs, and unfortunately, that often means deciding who stays and who goes.

This is why it’s so important to make sure the value you bring to your job is visible and undeniable. You don’t have to be perfect — you just need to make it clear that letting you go would create more problems than keeping you.

If your job requires specific skills, invest in sharpening them. Update your knowledge, take short courses, ask questions, and show that you’re growing instead of standing still. Skills are a form of job security. The more you can do — and the better you can do it — the harder it is for a company to justify starting with you when layoffs begin.

And if you work in a role that doesn’t require advanced or specialized skills, you can still stand out. Reliability, flexibility, and initiative matter just as much. Being the person who can cover an extra shift, help a colleague, learn a new task, or adapt quickly gives you a natural advantage. Managers notice who makes their life easier and who doesn’t. It’s often these small behaviours — showing up on time, being helpful, staying positive — that make a big difference when difficult decisions are being made.

When companies evaluate staff during layoffs, they quietly ask themselves: “Who brings the most to the table? Who solves problems? Who slows things down? Who can we not afford to lose?”

Your aim is to be on the side of that conversation where your absence would create a gap, not a convenience.

The truth is simple:

In uncertain times, the people who show value, reliability, and a willingness to grow naturally move higher on the “keep” list. It’s not about overworking or becoming a robot. It’s about being smart, intentional, and someone whose contribution is clearly felt.

This mindset not only protects you during layoffs — it also opens doors for promotions, better opportunities, and long-term career stability.

In an uncertain economy, depending on just one of anything is a risky strategy.

One job, one income stream, one supplier, one investment — it all becomes fragile the moment something goes wrong. And when the economy cools down, things do go wrong, often suddenly and without warning.

If all your income comes from a single job, you’re essentially standing on one leg. The moment that leg gets kicked out — layoffs, budget cuts, restructuring — you’re left with the same bills, the same mortgage, the same loans, but no safety net.

This principle isn’t just about jobs. It applies everywhere.

If you run a business, you already know that depending on a single supplier is like trusting one lifeline. If that supplier has a delay, raises prices, or goes out of business, suddenly your entire operation is at risk. Smart businesses always have backup suppliers — not because they expect disaster, but because they prepare for it.

Your investments work the same way. When you put all your money into one asset — only stocks, only real estate — you’re betting your financial stability on something you can’t control.

Markets crash. Companies fail. Industries shift. But diversification spreads the risk, so when one thing falls, something else holds you up.

This is the whole point of not putting all your eggs in one basket. Imagine your stocks drop — but you still have savings earning interest, maybe some real estate, maybe some bonds or gold. Each category behaves differently, which means not everything collapses at once.

The truth is simple:

When you depend on “one,” you put your life in someone else’s hands.

When you build multiple streams and diversify, you take that power back.

You don’t need five businesses or ten side hustles — even one small extra income stream can make a massive difference. Maybe it’s freelancing once a week, renting out a room for a few months, doing consulting on the side, selling something you no longer need, or turning a hobby into a small income. The amount doesn’t matter. What matters is building a buffer between you and uncertainty.

In today’s economy, stability doesn’t come from one big thing — it comes from several small ones working together. That’s how you protect yourself, reduce stress, and stay in control even when the world around you feels unstable.

When the economy slows, fear is usually the first reaction — fear of losing your job, rising prices, or the unknown. That fear often turns into blame: blaming the government, banks, your boss, or the wealthy — and envying Instagram lifestyles that are often funded by debt.

The thing is that blaming everyone and anything is not going to help you become financially stronger. Action will.

If you’ve lost your job or feel insecure about your stability, it’s completely normal to feel angry, sad, overwhelmed, or even embarrassed. You are going through a difficult emotional shift, and you need time to process it.

Let the emotions come up. If being upset for a few days helps you release pressure, allow it. This emotional detox is part of healing.

But you can’t stay in that state for too long.

At some point, you must stop, breathe, and look at your situation with clarity, because your next steps will determine how quickly you recover.

The truth is uncomfortable but freeing:

Most external forces are outside your control — but your financial decisions are not.

You cannot control layoffs, government decisions, the global economy, inflation, housing prices, interest rates, or food prices. But you can control how you respond:

– what you buy and what you stop buying,

– what you prioritize financially,

– what debts you choose to take on — or avoid,

– what income streams you build or explore,

– what skills you learn to increase your value,

– how you plan, save, and budget,

– your mindset, discipline, and decisions.

These choices will have a far bigger impact on your financial future than any external event.

Shift from reacting → to deciding

Before accepting a price, a purchase, or a lifestyle as “normal,” pause for a moment and ask:

* “Is this truly necessary?”

* “Is this an emotional decision?”

* “Am I doing this because of social pressure or habit?”

* “Does this help or hurt my long-term stability?”

Decide intentionally, rather than reacting to advertising, trends, or social pressure.

This mindset becomes ten times more important if you’ve been laid off, because every decision matters more when your income is uncertain.

Intentional decisions protect you.

Reactive decisions drain you.

Your power lies in the choices you make today — no matter what the economy is doing.

PART 2:

If You’ve Just Been Laid Off — Start Here

Losing a job can feel like the ground suddenly disappeared under your feet. One day you have structure, purpose, and routine — and the next, you’re waking up wondering what to do first.

This moment is emotionally dangerous, because things can go in two directions: it can become a turning point for growth, or it can spiral into stress, depression, and poor decisions.

That’s why your very first job after a layoff is simple: protect your mind.

When the routine disappears, it’s extremely easy to fall into a negative loop. People often feel worthless, anxious, or ashamed when they suddenly have too much time and no direction. This is where many go down the wrong path — spending money out of stress, isolating themselves, or losing confidence.

You need structure. You need purpose. And you need to train your mind during this transition.

Start by giving yourself a healthy routine — something that gets you out of bed and keeps your brain active. This could be:

– taking online courses that can benefit your career,

– learning skills you always postponed,

– reading or studying something that grows your confidence,

– setting small daily tasks to stay grounded.

This period can be incredibly powerful if you use it well. Now is the perfect time to focus on your personal finances, understand your relationship with money, and strengthen your long-term habits.

And this part is crucial:

Pause before spending. Pause before accepting “normal.” Pause before following trends or what others are doing.

When you’ve just lost your job, the last thing you need is to dig yourself deeper into financial trouble because of social pressure — buying a new iPhone because “everyone else has it,” or taking on credit card debt to buy clothes that make you look successful on the outside while your bank account suffers.

Remember: The system profits when you’re stressed and uninformed. Banks profit from your debt. Corporations profit from your impulses. Credit card companies profit when you overspend.

But none of them profit when you’re calm, educated, and intentional.

Your responsibility right now is to slow down, think clearly, and make decisions that protect your future self — not impress strangers.

After you stabilize your mindset, the next step is urgent: deal with your debt.

Debt is one of the biggest risks during a recession because when your income stops, your payments don’t.

Losing a job exposes the truth many people ignore: debt removes your flexibility. It forces you into bad decisions, limits your options, and can destroy your financial safety faster than anything else.

There is a quote that sums it up perfectly:

“Debt is like a ticking time bomb. You don’t notice it when things go well, but when things go bad — and they always go bad eventually — debt will destroy you.”

I’ve seen smart people lose everything not because they invested badly, but because they borrowed too much. I’ve seen businesses collapse because they depended too heavily on loans.

Debt makes you vulnerable in ways you won’t understand until something goes wrong.

High-interest debt is the real enemy:

In Iceland today:

– credit-card interest rates are typically around 14–16%,

– car loans generally sit around 10–11%.

No investment beats that.

Paying off high-interest debt provides the highest guaranteed return you can possibly get. If you have such loans, eliminating them should be your top priority. Not saving, not investing — debt comes first. The only exception is building a small emergency fund — enough to cover unexpected expenses so you don’t have to borrow while paying down debt.

Why people get trapped in debt:

A painful truth always shows up during economic downturns:

Most people didn’t borrow money because they needed something — they borrowed because of insecurity, social pressure, or the need to look successful.

People take loans to:

– impress others,

– keep up with their friends,

– appear successful,

– escape boredom,

– feel normal,

– avoid feeling left out.

But in uncertain times, these decisions turn dangerous.

Your responsibility now is not to impress anyone. Your responsibility is to protect your stability.

Your action plan:

– Pay high-interest debt first. Credit cards, personal loans, and auto loans — anything above 10% — are eating your future. Make minimum payments on all your other loans to avoid penalties and protect your credit.

– Avoid taking on new loans, especially for lifestyle upgrades like cars, tech, or furniture.

– Instead of going deeper into debt, focus on saving as much as you can.

Remember what the system really is:

When you walk into a bank and ask, “Can I afford this?”, remember that their goal is to sell you a loan. A bigger loan earns them more money.

Your financial stability is not their priority. This doesn’t make them evil — it just means you need to be the one protecting yourself.

If you follow the crowd, you end up where the crowd ends up — stressed, indebted, and living paycheck to paycheck.

But if you pause, question, and act intentionally, even a layoff can become the moment where your financial life becomes stronger than ever.

When you lose your job, the first question that determines how stressed you will be isn’t “When will I find a new job?”

The real question is: “How long can I survive without income? / How long can I manage on reduced income?”

1. Why your emergency fund matters more now than ever:

Your emergency fund is more than just money in the bank — it’s stability, control, and peace of mind. It exists for moments like this, and hopefully you have it fully funded in a high-yield savings account that’s easily accessible.

When income drops or you’re relying on unemployment benefits, that financial cushion turns a stressful situation into a manageable one. Without it, even a short period of unemployment can push you deeper into debt.

Now is the time to let your emergency fund do its job. Use it intentionally to cover essentials, lower your stress, and give yourself the breathing room you need to find your next opportunity. That’s exactly what it was built for.

And don’t feel guilty about spending it — an emergency fund isn’t meant to sit untouched forever. It’s there to protect you when life becomes unpredictable.

Focus on using it wisely, avoiding new debt, and stabilizing your situation. Once you’re employed again, you can rebuild it step by step. For now, let your emergency fund support you so you can stay secure and make clear decisions moving forward

2. Cutting expenses = immediate power:

In a recession, cash flow is your strongest form of protection. The money you keep matters just as much as the money you earn. When you control your outflow, you immediately strengthen whatever inflow you still have. Cutting expenses isn’t punishment — it’s strategy. It buys you time, reduces stress, and gives you options you wouldn’t have otherwise.

Small lifestyle adjustments today can prevent months of financial pressure later. Focus on practical, high-impact actions: cook at home instead of eating out, stick to a grocery list, and delay unnecessary upgrades. Even subtle changes, like unfollowing influencers who trigger FOMO, help you resist pressure to spend on things that add nothing to your long-term stability.

In a recession, frugality isn’t just smart — it’s self-defense. Every króna you save stretches your safety net and buys you time to get back on your feet.

3. Stop flex spending:

Flex spending is about ego — spending to impress others or signal success. But this mindset of “I worked hard, I deserve this” is extremely dangerous when income is uncertain. Now is not the time to buy things for status or instant gratification. Ego-driven purchases are the first to drag people into debt during economic downturns.

As Morgan Housel puts it:

“Saving money is the gap between your ego and your income, and wealth is what you don’t see.”

Focus your spending on essentials: housing, food, utilities, and insurance. Eliminate waste wherever possible, such as impulse purchases, emotional shopping or lifestyle upgrades. Skip items you want only because they’re new or trending.

Remember: Corporations profit when you make impulsive or status-driven purchases.

Protect yourself by spending intentionally, not to keep up appearances.

4. Be strategic with your living situation:

Housing costs are often your largest expense — and your biggest risk if you lose your job. If you live alone, rent can quickly become a threat.

Practical ways to reduce this risk include renting out an unused room or sharing expenses with a roommate, partner, or friend. Even a few months of shared costs can dramatically extend your financial runway.

A recession is not the time to let pride drain your bank account. It’s the time to be resourceful, strategic, and focused on protecting your financial stability.

Financial survival isn’t just about money — it’s about psychology, habits, and the people around you. It’s about the mindset you carry every day.

When income becomes uncertain, emotions run high. It’s easy to compare yourself to others who seem to be “winning,” scrolling social media and feeling like everyone else is ahead. But appearances are deceiving.

Remember: People show their lifestyle, not their struggles, and many who look the richest are often the ones struggling the most.

Too often, people mistake “looking rich” for actually being wealthy.

2025 and 2026 are not the years to buy a flashy car, move into a more expensive home, or take on a mortgage just for an Instagram photo. Stop following the herd — the herd is broke.

1. Choose your circle wisely:

As the famous quote goes, “You are the average of the five people you spend the most time with.”

This becomes extremely important when it comes to your personal finances, especially if you get laid off.

If your circle pressures you to spend, discourages your goals, or drains your energy, it’s time to set boundaries — or step back. In uncertain times, the people around you have a direct impact on your financial habits.

But if your friends save, invest, and plan for the long term, you’ll naturally rise to their level. But if they overspend, chase instant gratification, or rely on debt, you’re likely to mirror their behavior.

Be deliberate about who influences your decisions. Surround yourself with people who make you smarter, not poorer. The habits you build during tough times are the ones that will protect you for life.

2. Communicate your goals

If you’re trying to save, pay down debt, or make smarter financial choices, speak up. Real friends will understand when you say:

– “I’m cutting back on eating out.”

– “I’m trying to save more.”

– “I’m paying off debt.”

Fake friends may take offense, but real friends support your growth.

If you’re in a relationship, align financial goals with your partner. Treat money management as a team effort — you’ll achieve far more together than alone.

Losing your job is stressful, and it’s natural to feel fear about the future. One of the most dangerous mistakes you can make now is panicking and touching your long-term investments.

A recession — or sudden unemployment — amplifies fear, and fear can interrupt the very force that builds wealth over time: compounding.

Selling your investments when the market feels unstable locks in losses and can erase years of growth. Your portfolio is designed to weather decades, not weeks of instability. Unless you absolutely must access cash to cover essentials, leave your long-term investments untouched.

At the same time, it’s common to feel the urge to ‘make back’ losses quickly. Many chase risky stocks, speculative crypto, or trending investments out of fear of missing out. This is exactly the wrong move. Emotional decisions in uncertain times are your worst enemy.

After a layoff, gambling with your money is something you should never do. Forget hot tips, hype, and quick wins. Your priority is to protect what you have, stay liquid, keep cash accessible for opportunities, and focus on safe, steady returns.

True wealth is quiet. Security is quiet. Stability is quiet.

It doesn’t come from impulsive decisions, risky bets, or showing off.

Wealth comes from controlling your spending, avoiding debt, saving consistently, investing wisely, diversifying, staying patient, and maintaining strong financial habits even when life feels uncertain.

As Morgan Housel says, “Wealth is what you don’t see.”

After a layoff, this mindset is more important than ever. Choose stability over appearances, long-term thinking over short-term impulses, and discipline over emotion.

The people who survive — and even thrive — in economic downturns are those who stay calm, stay smart, and stay disciplined.

1. See change as opportunity:

Many people think recessions are only about fear and loss — but that’s not the full picture.

Every economic downturn has created some of the biggest opportunities. People pivot careers, start new businesses, or turn to freelancing. Companies restructure, new industries appear, and assets often become cheaper.

Opportunities don’t disappear just because the economy slows down — they shift. Your job is to position yourself on the right side of that shift. Whether times are good or bad, someone is always benefiting. Make sure you’re not the one sitting on the sidelines.

2. Smart people prepare, so they can act:

When the economy dips, financially prepared people aren’t panicking. They’re buying undervalued assets, improving their skills, or stepping into gaps that others leave behind. Recessions create openings for those who are paying attention.

3. Invest in your financial education:

Knowledge becomes your greatest asset in uncertain times. Read books, take courses, follow reliable personal finance educators, or learn from people who have already built the level of wealth and stability you want. Ask how they built their financial foundation, what mistakes they made, and what they would do if they were starting again today.

A good mentor can help you avoid costly mistakes and can guide you when you’re uncertain or tempted to fall back into old habits.

Bottom Line

This article isn’t meant to overwhelm you. Its goal is to highlight practical ways to prepare yourself financially and emotionally, whether you still have your job or have recently been laid off. You don’t need to follow every recommendation; even taking action on a few strategies can put you far ahead of most people.

Of course, I don’t know your exact financial situation, and not every approach will suit everyone. Consider this a menu of options — ideas you can adapt to your own circumstances to protect and strengthen your financial position. Pick the strategies that fit your situation, and start taking action today.